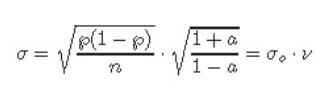

Variance Modulating Factor

Variance effect in a first-order, two-state Markovian process with equal self-transition

probabilities, p.

Variance

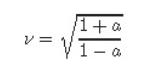

Variance Modulating Factor

Variance effect in a first-order, two-state Markovian process with equal self-transition

probabilities, p.

Variance

Variance Modulating Factor

Variance effect in a first-order, two-state Markovian process with equal self-transition

probabilities, p.

Variance

Variance Modulating Factor

Variance effect in a first-order, two-state Markovian process with equal self-transition

probabilities, p.

Variance